Page 129 - Quick Insights Book 2022

P. 129

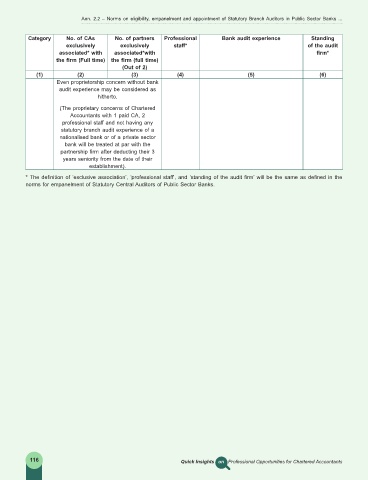

Ann. 2.2 – Norms on eligibility, empanelment and appointment of Statutory Branch Auditors in Public Sector Banks ...

Category No. of CAs No. of partners Professional Bank audit experience Standing

exclusively exclusively staff* of the audit

associated* with associated*with firm*

the firm (Full time) the firm (full time)

(Out of 2)

(1) (2) (3) (4) (5) (6)

Even proprietorship concern without bank

audit experience may be considered as

hitherto.

(The proprietary concerns of Chartered

Accountants with 1 paid CA, 2

professional staff and not having any

statutory branch audit experience of a

nationalised bank or of a private sector

bank will be treated at par with the

partnership firm after deducting their 3

years seniority from the date of their

establishment).

* The definition of ‘exclusive association’, ‘professional staff’, and ‘standing of the audit firm’ will be the same as defined in the

norms for empanelment of Statutory Central Auditors of Public Sector Banks.

116 Quick Insights on Professional Opportunities for Chartered Accountants